RCM Managed Asset Portfolio - Q3 2021

RCM Managed Asset Portfolio

By Christopher Chiu, CFA

When Will the Fed Move?

RCM Update

Some news. We now manage a mutual fund in the Catalyst Mutual Fund family focused on selecting high quality growth stocks. It uses the same investing style and fundamental and technical analysis that our current equity programs at RCM are based on. It is called the Catalyst Pivotal Growth Fund and its symbol is BUYIX. With that bit of news out of the way, on to the quarterly letter.

Tapering and Its Effects

We continue to monitor risks in the equity and bond market. Right now, we are in the middle of an economic expansion, and the most obvious risk to these markets is a Fed driven rise in rates. The biggest factor that will push the Fed to raise rates is if inflation proves to be more than transitory. I’m not arguing whether there is inflation in the short term. There almost certainly is. The CPI is going to exceed 4% for the year. But the important question is whether we continue to get a 4% rise in the CPI next year and in the months following. If so, then there is almost certainly going to be a consistent policy response. And the consequences of multiple rate raises would be a challenging period of revaluation of equities and bonds.

Despite the recent inflation narrative, the prices of most bonds have still not fallen off dramatically. There’s a still chance they may, either from consistent inflation or from the tapering program enacted by the Fed to begin to fend off said inflation. The last time there was a tapering of QE was in 2013. This was the period known infamously as the taper tantrum. During that time riskier bonds and even investment grade corporate sold off 8-10% from peak to trough in a period of three months, before the Fed even made a single move! Then bonds regained that loss over the next 18 months as the taper tantrum turned out not to affect the long-term pricing of these assets. It’s not clear the bond market would react in the same way with tapering this time around. (We simply don’t have enough history of QE and tapering to know for certain.) But so far given the chance, they have not done so. If bonds were to start selling off, we would move to lower volatility bonds and bonds less affected by rates.

Keep in mind, tapering is not the raising of rates. It’s simply an ending of the QE/Fed bond buying program. But it is a step in draining excess liquidity from the financial system. You may have already seen the Fed doing this lately with the reverse repo program. Draining overall liquidity from the financial system will be a multistep process and each time it occurs there will seem to be a risk to assets. But unless there is a full-blown recession, asset prices generally recover. From my experience with the last economic cycle, it seems like the draining of excess liquidity will occur in the following sequence.

1. Reverse repo

2. Fed signaling of tapering and the actual tapering (2013-14 the last time)

3. Fed signaling and formal raising of rates (2017-18 the last time)

What results after a series of Fed raises (step 3) is often a yield curve inversion, after which the Fed usually takes a pause in its raising of short-term rates. Then after this pause there is usually a sigh of relief and a final boom in bond and equity prices. This is what occurred in 2007 and 2019. Then eventually there is a recession when asset prices experience a large drawdown and take a longer time to recover.

All of this will take a long time to play out (at least three years and probably more), during which time investors will benefit from continuing to be in the equity market. And there is some evidence to suggest that there are reasons for the Fed to act more slowly than one might anticipate. We will discuss these in the next section.

Status of the Current Economic Cycle

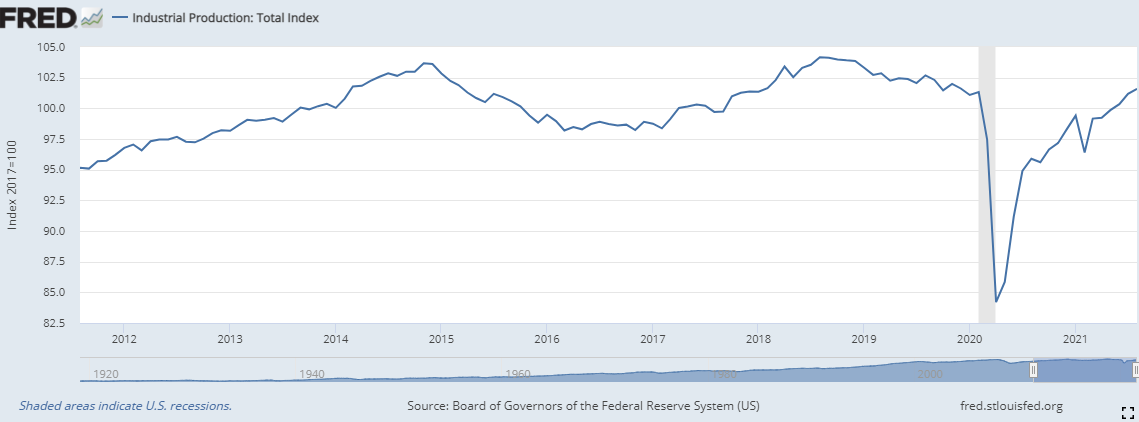

There are counter forces that would limit the Fed from raising rates as quickly as people might think. Some current economic data isn’t all that robust. It certainly doesn’t show an economy running at full capacity. For example, there currently is plenty of slack in industrial production. Note the current gap below the red line.

It wasn’t until industrial capcity reached its max in middle of 2014 during the last economic cycle that the Fed entertained raising the Fed Funds rate in 2015. We have yet to reach that level once in this economic cycle.

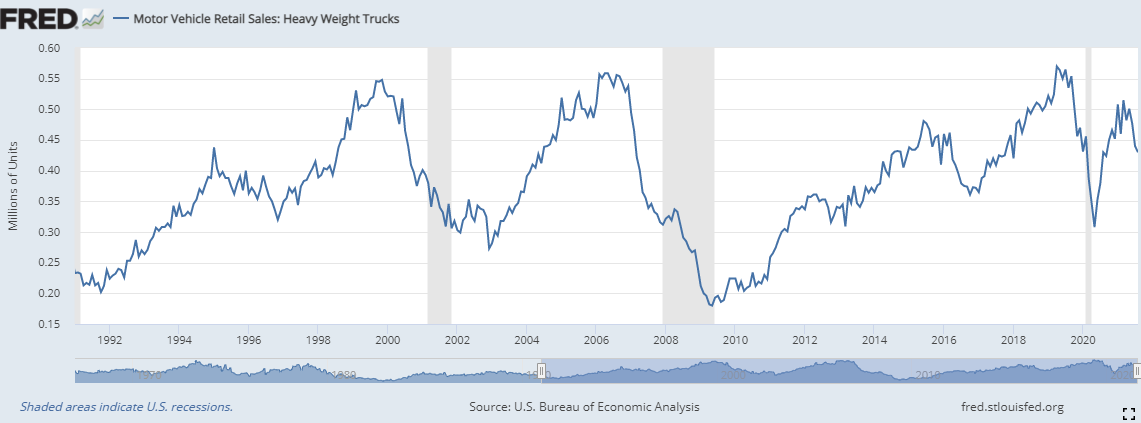

Further, though the economy is still expanding and will continue to expand, it will do so unevenly. A good example of this unevenness is a recent slowdown in heavy truck sales, likely caused by higher prices.

So while higher prices do show strong demand, they also carry with them effects that tamper their own potency. Higher prices show strong demand, but higher prices also mean the marginal buyer will be put off by higher prices, which leads to fewer sales. Slow down effects like this would also discourage the Fed from raising rates as quickly as people might anticipate.

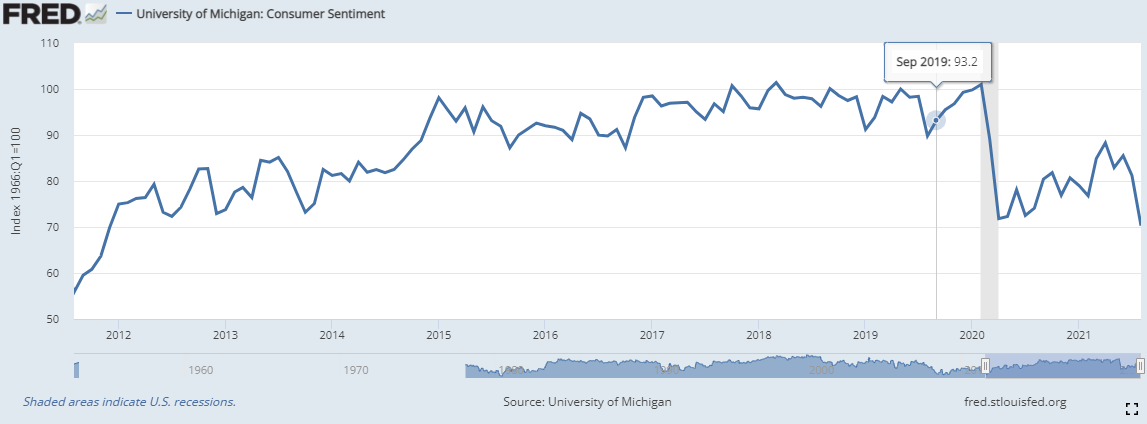

Higher prices have also had a similar dampening effect on consumer sentiment. The University of Michigan Consumer Sentiment survey showed a recent dip in consumer confidence.

While the general trajectory for consumer sentiment is upward and to the right until the economic cycle comes to an end, the sentiment index gets there in an uneven manner with a number of dips along he way. Note, peak consumer sentiment is generally around 100 and we have yet to reach that level at all during this economic cycle.

Speaking with a colleague in the office recently, I noted that the Fed can do away with most of these troublesome instances of higher prices, higher costs, supply shortages, container ship gluts, and all the other headline inflation items. The simple solution to fix all of these is for the Fed to immediately raise the Fed Funds rate. But to do so would immediately slow the economy and would the Fed really do that when the economy has not reached full capacity? It would not be in its character to do so, at least not by observing the pattern of its policies over the last thirty years. But then again, we haven’t seen inflation like this for at least the last thirty years.